Navigating Insurance can be complex and overwhelming, especially with the variety of plans and options available. Working with a broker can significantly simplify this process and offer several benefits

Understanding Medicare Supplement Plans

Medicare Supplement plans, also known as Medigap, are insurance policies designed to fill the gaps in Original Medicare (Part A and Part B) coverage. These plans are offered by private insurance companies and can help cover out-of-pocket costs such as copayments, coinsurance, and deductibles. Here’s a comprehensive look at what Medicare Supplement plans entail and how they can benefit you.

What Are Medicare Supplement Plans?

Medicare Supplement plans are standardized insurance policies that work alongside Original Medicare. They are designed to cover some of the healthcare costs that Original Medicare does not, such as:

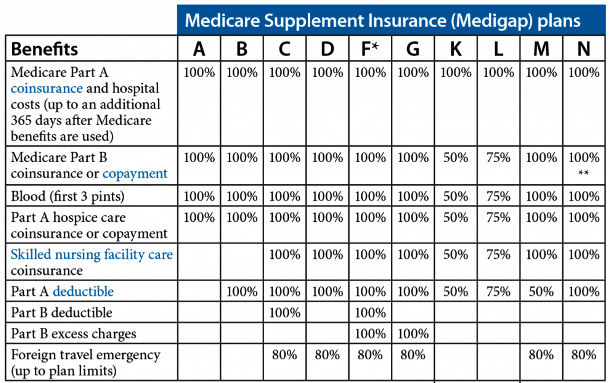

Types of Medicare Supplement Plans

There are ten standardized Medigap plans available in most states, labeled A through N. Each plan offers a different level of coverage, but the benefits of each plan are the same regardless of the insurance company offering it. Here’s a brief overview of some of the most common plans:

Enrollment and Eligibility

To be eligible for a Medicare Supplement plan, you must be enrolled in Medicare Part A and Part B. The best time to purchase a Medigap policy is during your Medigap Open Enrollment Period, which is a six-month period that starts the month you turn 65 and are enrolled in Part B. During this period, you have a guaranteed issue right, meaning you can buy any Medigap policy sold in your state without medical underwriting.

Costs of Medicare Supplement Plans

The cost of a Medigap policy varies depending on several factors, including the plan you choose, your age, gender, location, and the insurance company. Generally, Medigap policies have higher premiums but lower out-of-pocket costs compared to Medicare Advantage plans. It’s important to compare different plans and insurance companies to find the best coverage at the most affordable price.

Benefits of Medicare Supplement Plans

Medicare Supplement plans offer several advantages:

Key Considerations

When choosing a Medicare Supplement plan, consider the following:

Medicare Supplement plans can provide valuable coverage and peace of mind by helping to manage healthcare costs not covered by Original Medicare. By understanding your options and carefully comparing plans, you can find the coverage that best fits your needs and budge

Have any Question? Ask us anything, we’d love to answer!

We’re here to listen: